TED and Graves’ Disease: Three Waves, One Autoimmune Root

91 TED and Graves’ disease assets mapped across three emerging treatment waves. The largest wave now attacks the autoimmune root, not just the orbit.

Download the Visual

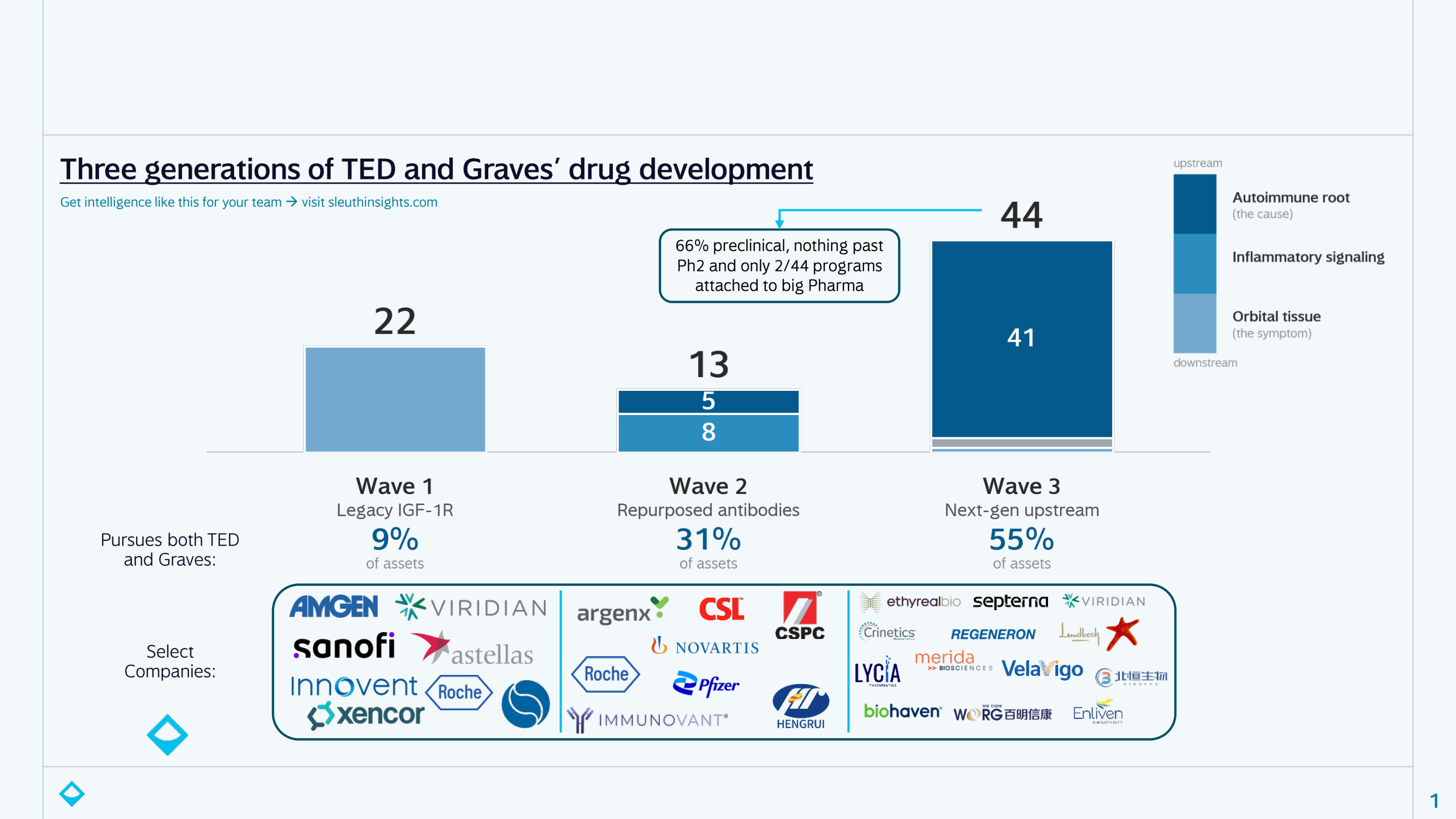

The landscape of TED and Graves’ disease targeting drugs has quietly shifted since Tepezza launched ~6 years ago. I used Sleuth to aggregate 91 assets in development across both diseases and sorted by where in the disease it intervenes. Three generations have recently emerged:

- Wave 1 – legacy IGF-1R (22 assets): blocks the same target Tepezza validated at the orbit

- Wave 2 – repurposed antibodies (13): FcRn and anti-inflammatory antibodies borrowed from other autoimmune diseases

- Wave 3 – next-gen upstream (44): attacks the autoimmune root itself, mostly the TSH receptor that drives both conditions

Wave 3 is now the largest class, with lots of capital flowing in (Ethyreal launched last week with $101M, as just one recent example):

- 93% of programs attack the root, rather than the eye

- 55% are built for both Graves’ and TED at once, vs. 9% of legacy programs

- It’s early: ~66% are preclinical, there’s nothing past Phase 2 and only 2/44 carry any big Pharma involvement (good chance we see more BD over the next 18 months as we get real clinical data on TSHR-directed assets)

The bet is that since Graves’ and TED run on the same autoantibodies, they shouldn’t be treated as separate problems. Blocking the TSH receptor means you could get one drug that addresses both, potentially before TED ever develops. That makes the opportunity much bigger than “a better Tepezza” (~$2B in annual sales) but rather “the first disease-modifying therapy for Graves’”.

But even the core TED opportunity has room – the TAM is closer to $5B with ~80% of moderate-to-severe patients still untreated. Tepezza works well, but its profile has issues: 8 IV infusions over 6 months, ~$500K treatment course and a hearing impairment signal with real-world reports as high as ~65-81% (vs ~10% in trials), which has drawn a FDA label warning and some litigation headaches for Amgen. That’s why nearly every emerging program is sub-Q or oral, and why mechanisms with lower hearing risk are positioning for earlier-line treatment or combo use.

If you’re a CEO, Strategy, or BD lead, a landscape like this is just step one. Sleuth delivers the work you’d otherwise hand to a consultant: continuous monitoring across dozens of spaces, opportunity and positioning strategy, and BD enablement from target to diligence to intro, all on demand. Get in touch to learn more.

And comment below for a short primer that goes a level deeper than the post: the full clinical stage landscape and a few other cuts that didn’t fit here.